Idealliance's Andrew Paparozzi on the Commercial Printing Industry's Outlook

(Click on chart to enlarge)

So much is happening in the commercial printing industry that it’s hard to say with confidence what’s ahead. But one thing is very likely: In terms of overall business conditions, 2017 will look a lot like 2016. And one thing is certain: History’s third great economic revolution will continue to transform the industry, rewarding the prepared and punishing the unprepared — no matter how big, established or successful the unprepared have been.

Commercial printing’s performance heading into 2017 can best be described as an upturn that often hasn’t felt like an upturn. Activity picks up but doesn’t stay up, creating a plodding advance with limited pricing power, persistent pressure on margins, and the heightened uncertainty that complicates hiring and investment decisions and makes effective planning even more challenging.

The reasons why start with the digitization of communication, which has deeply depressed demand for the industry’s core services. For example, between 2000 and 2014 sales of commercial lithographic printing declined by $23.5 billion — from $59.3 billion to $35.8 billion — or triple the $7.7 billion increase in commercial digital printing sales, according to the U.S. Department of Commerce. No industry recovers quickly from that kind of hit.

The economy is also high on the list. GDP has grown an average of just 2.2% per year since the end of the Great Recession, well below the 3.4% annual growth during the quarter century prior to the downturn. No one knows why. We do know that it matters: The difference between the economy growing an average of 2.2% rather than 3.4% per year over the past six years approaches $1.0 trillion of final goods and services that didn’t get produced, promoted, etc.

Era of Diversification, Consolidation

We also know that the commercial printing industry is adjusting to these realities through diversification — companies surveyed by Idealliance expect something other than lithography to provide more than 52.0% of their sales by the end of 2017, up from 26.0% in 2007— and consolidation —the number of commercial printing establishments has declined by 6,600, or 21.5%, since 2007.

So print’s outlook comes down to this: Does anything suggest the pace of adjustment will accelerate significantly or the economy will step back up to 3.0%+ growth during the next 12 months?

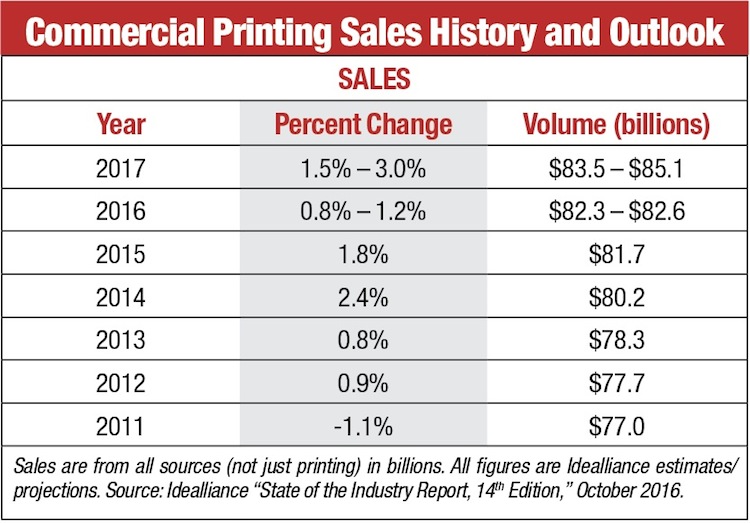

Idealliance’s answer is “no,” which is why we expect 2017 to look a lot like 2016 for commercial printing. As the table shows, our current forecast has the industry’s total sales (all sources) growing 1.5–3.0% next year, after growing approximately 1.0% this year. That would lift dollar volume to more than $83.0 billion — nearly 10.0% above the 2011 low, but still 14.0% below pre-Great Recession levels.

We aren’t alone in expecting more of the same: “State of the Industry” participants tell us that their biggest concerns — creating and maintaining revenue growth, uncertain economy/business conditions, rising costs (particularly health care) in markets that are still very resistant to price increases and maintaining profitability — were their biggest concerns heading into 2017.

Now for the rest of the story. Call it the “Information Revolution,” the “Digital Revolution,” the “Communication Revolution” or anything you want. By any name, it is redefining the commercial printing industry’s (and every other industry’s) customers, competitors, critical skills and value proposition, and eroding traditional markets and creating new ones. The recently published Idealliance “State of the Industry Report, 14th Edition” presents several ways to make the revolution an opportunity rather than a threat. Among them:

- Learning and doing. During an economic revolution both the returns to making the right decisions and the costs of making the wrong ones rise rapidly. Superior decisions are founded in superior knowledge of what’s happening inside and outside our companies, why it’s happening and what to do about it. We have to capture that knowledge and be agile enough to translate it quickly and efficiently into action.

- Urgency and discipline. It isn’t enough to set priorities for our companies. We have to create urgency around our priorities by reinforcing companywide that they are not options, filler for the strategic plan or nice things to do if we ever get the time. They are necessities that must be addressed — now. And we have to cultivate the discipline — again, companywide — to address them without being lax, distracted or sloppy in our execution.

- Pick our shots carefully. There’s plenty of opportunity in the commercial printing industry. Just ask the Idealliance “State of the Industry” participants, whose list of growth prospects includes:

o More than 20 products, with direct mail; display advertising; promotion; packaging; and wraps, banners and signs cited most frequently.

o More than 10 processes, led by variable-data color digital, inkjet, static-data digital color and wide-format digital printing.

o More than 20 services, ranging from fulfillment to 1:1 cross-media marketing to strategy and planning to mobile advertising/applications to video for the Web.

The challenge is identifying what really is an opportunity given a specific company’s unique resources, capabilities and goals because margins for error have gotten too thin to chase bad fits. Tools such as the “opportunity evaluation matrix” and “real vs. ideal analysis” help us decide by answering questions such as:

o Who, exactly, will our customers be? How much revenue can we expect from them — i.e., what’s the true size of the opportunity?o Who, exactly, will our customers be? How much revenue can we expect from them — i.e., what’s the true size of the opportunity?

o What are the up-front costs? How much will we have to invest just to get in the game?

o What skills are required? Do we have the expertise — technical, sales, marketing, leadership, etc. — necessary to make the option work? If not, how will we acquire it?

o Who’s the competition? Companies like our own? Or a new breed of competitor with whom we have little experience?

- Challenge our key business assumptions. When our environment changes but our assumptions don’t, we’re headed for big trouble. Therefore, we should regularly ask: What exactly are we assuming about our clients, markets, competition and resources? Which assumptions are still valid and which are no longer valid?

- Read “weak signals.” They’re the trends and issues we’re hearing about but not yet experiencing. Keep a list of them. And never make the deadly mistake of assuming that, because something isn’t affecting us today, it isn’t going to affect us tomorrow.

Like all revolutions, the revolution redefining the printing industry will create winners and losers. The difference between the two will be superior market intelligence, agility, execution and discipline — not company size, ownership structure or services offered. The question everyone in the industry should be asking: What will we do in 2017 to be one of the winners?

Click here for the 2016 Printing Impressions 400 ranking (Opens as a PDF).

Andrew Paparozzi serves as chief economist at PRINTING United Alliance. He is the author of the recently completed Idealliance "State of the Industry Report, 14th Edition," which was sponsored by Canon U.S.A.