Donnelley Financial Reports Q4, Full-Year 2017 Results, Issues 2018 Guidance

CHICAGO - March 1, 2018 - Donnelley Financial Solutions reported financial results for the fourth quarter and full year 2017.

Highlights:

Click to enlarge chart

Daniel N. Leib

“I am pleased with our results for 2017, our first full year as a standalone company,” said Daniel N. Leib, Donnelley Financial’s president and CEO. “Revenue increased by $21 million, driven by growth in Investment Markets, Language Solutions and International, while softer than expected transactional activity resulted in a modest decline in U.S. capital markets. The revenue growth we achieved, coupled with aggressive cost management, drove $63.6 million of free cash flow in 2017, most of which was used to reduce the Company's debt. Within the first five quarters of the spin-off from R.R. Donnelley, we have reduced our total debt by nearly $180 million, ending 2017 with gross leverage of 2.6x. In addition, we ended the year with $52 million of cash.”

Leib continued, “In light of our strengthened financial position, the market opportunities we see and the benefits of the recently announced tax legislation, we will increase our investments in 2018 to drive long-term growth. Our targeted gross leverage range remains in the range of 2.25x to 2.75x.”

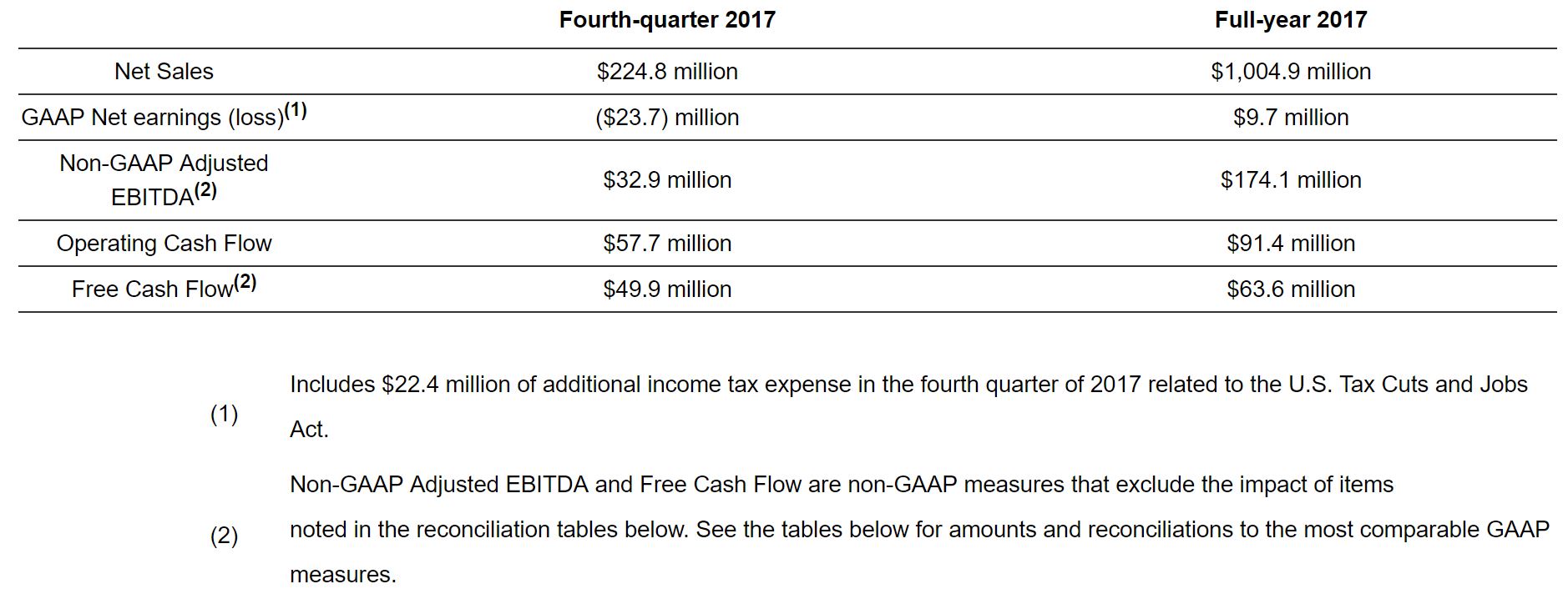

Net Sales

Net sales in the fourth quarter of 2017 were $224.8 million, an increase of $3.8 million, or 1.7%, from the fourth quarter of 2016. After adjusting for changes in foreign exchange rates, organic sales increased 1.0% from the fourth quarter of 2016 driven primarily by growth in transactional, compliance and Venue revenue within U.S. Capital Markets, which was partially offset by declines in U.S. Investment Markets and International.

GAAP Earnings (loss)

Fourth-quarter 2017 net loss was $23.7 million, or $0.71 per diluted share, compared to net loss of $0.8 million, or $0.02 per diluted share, in the fourth quarter of 2016. The fourth-quarter 2017 net loss included additional income tax expense of $22.4 million, or $0.67 per diluted share, related to the impact of the U.S. Tax Cuts and Jobs Act. The fourth-quarter net loss included after-tax charges of $28.4 million and $4.9 million in 2017 and 2016, respectively, all of which are excluded from the presentation of non-GAAP net earnings. Additional details regarding the amount and nature of these and other items are included in the attached schedules.

Non-GAAP Adjusted EBITDA and Net Earnings (loss)

Non-GAAP adjusted EBITDA in the fourth quarter of 2017 was $32.9 million, compared to $27.7 million in the fourth quarter of 2016. Non-GAAP adjusted EBITDA margin in the fourth quarter of 2017 was 14.6%, 210 basis points higher than in the fourth quarter of 2016. The increase in non-GAAP adjusted EBITDA and non-GAAP adjusted EBITDA margin was primarily driven by company-wide cost reductions and increased activity within U.S. Capital Markets, partially offset by reduced activity within International and U.S.Investment Markets, as well as higher employee-related expenses.

Non-GAAP net earnings totaled $4.7 million, or $0.14 per diluted share, in the fourth quarter of 2017 compared to non-GAAP net earnings of $4.1 million, or $0.13 per diluted share, in the fourth quarter of 2016. Reconciliations of net earnings to non-GAAP adjusted EBITDA and non-GAAP net earnings, as well as non-GAAP adjusted EBITDA margin, are presented in the attached schedules.

Impact of the U.S. Tax Cuts and Jobs Act

The Company recorded additional income tax expense of $22.4 million, or $0.67 per diluted share, in the fourth quarter of 2017 related to the impact of the U.S. Tax Cuts and Jobs Act. The additional income tax expense represents the Company’s initial estimate of the transition tax imposed on accumulated foreign earnings and the remeasurement of the Company's net deferred tax asset.

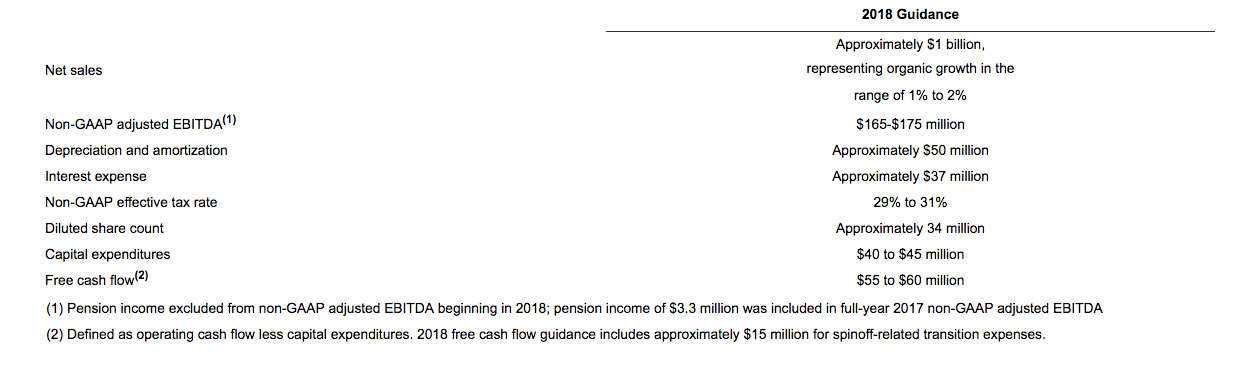

2018 Guidance

The Company provides the following full-year guidance for 2018, which includes increased operating expense and capital expenditures related to investments targeted toward driving long-term revenue growth:

Click to enlarge chart

Certain components of the guidance given above are provided on a non-GAAP basis only, without providing a reconciliation to guidance provided on a GAAP basis. Information is presented in this manner, consistent with SEC rules, because the preparation of such a reconciliation could not be accomplished without “unreasonable efforts.” The Company does not have access to certain information that would be necessary to provide such a reconciliation, including non-recurring items that are not indicative of the Company’s ongoing operations. Such items include, but are not limited to, restructuring charges, impairment charges, spinoff-related transaction expenses, acquisition-related expenses, gains or losses on investments and business disposals and other similar gains or losses not reflective of the Company's ongoing operations. The Company does not believe that this information is likely to be significant to an assessment of the Company’s ongoing operations, given that it is not an indicator of business performance.

Source: Donnelley Financial Solutions.

The preceding press release was provided by a company unaffiliated with Printing Impressions. The views expressed within do not directly reflect the thoughts or opinions of Printing Impressions.

- Companies:

- Donnelley Financial Solutions