Pitney Bowes Reports Financials for Full Year, Q4 2015 with a Decline in Revenue

STAMFORD, Conn.—February 2, 2016—Pitney Bowes Inc., a global technology company that provides products and solutions that power commerce, today reported financial results for the full year and the fourth quarter 2015. The company also provided annual guidance for 2016.

Full-Year 2015:

- Revenue of $3.6 billion, a decline of 3 percent on a constant currency basis and 6 percent on a reported basis

- Adjusted EPS of $1.75; GAAP EPS of $2.03. EPS includes a $0.07 per share negative impact of foreign exchange during the year.

- SG&A expenses of $1.3 billion, a reduction of $98 million year-over-year

- Free cash flow of $456 million; GAAP cash from operations of $515 million

- Repurchased $135 million of common stock; reduced debt by $280 million and refinanced $110 million of debt

Fourth Quarter 2015:

- Revenue of $937 million, a decline of 2 percent on a constant currency basis and 5 percent on a reported basis

- Adjusted EPS of $0.48; GAAP EPS of $0.44. EPS includes a $0.02 per share negative impact of foreign exchange during the quarter.

- SG&A expenses of $341 million, a reduction of $6 million

- Free cash flow of $157 million; GAAP cash from operations of $164 million

- Repurchased $35 million of common stock and refinanced $110 million of debt using funds from a $150 million bank term loan

“We made substantial progress against our strategic objectives in 2015 and entered 2016 in a stronger position," said Marc Lautenbach, president and CEO, Pitney Bowes. “In the fourth quarter, most of our businesses performed in-line with our long term expectations; however, our Software business fell short of what we had expected. As we look forward, we continue to feel good about where we are in our transformation and our ability to deliver long term value to our shareholders.”

Full Year 2015 Results

For the full year, revenue totaled $3.6 billion, a decline of 3 percent on a constant currency basis and 6 percent on a reported basis when compared to the prior year. As part of its previously announced go-to-market strategy, in 2014 the company exited a non-core product line in Norway and transitioned from a direct sales model to a dealer sales network in six smaller European markets for the International Mailing and Production Mail segments. For comparative purposes, revenue for 2015 would have declined 2 percent on a constant currency basis when revenue in the current and prior years is adjusted for the impact of these divested revenues.

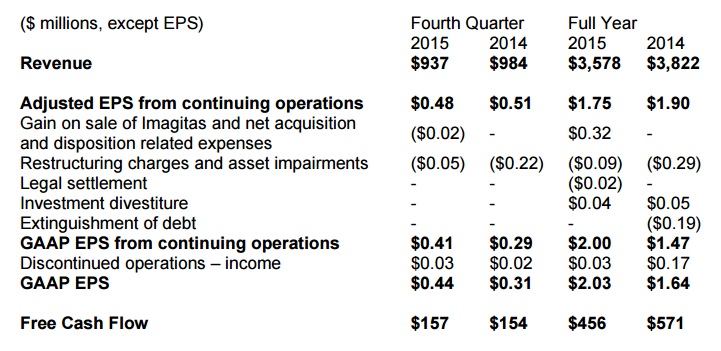

On a Generally Accepted Accounting Principles (GAAP) basis, earnings per diluted share were $2.03.

Adjusted earnings per diluted share from continuing operations were $1.75 and exclude:

- $0.32 which includes a gain from the sale of Imagitas of $0.44 and net acquisition and disposition related expenses of $0.12;

- $0.09 of restructuring and asset impairment charges;

- $0.02 of legal settlement expense;

- $0.04 benefit related to a previous investment divestiture;

- $0.03 of income from discontinued operations.

Earnings per share for the year were reduced by $0.07 due to the impacts of foreign exchange. Additionally, adjusted earnings per share were adversely impacted by the 33.5 percent tax rate, which was at the high-end of the company’s guidance range primarily due to a greater percentage of U.S. sourced income.

Free cash flow for the year was $456 million and the company generated $515 million of cash from operations on a GAAP basis. In addition to investing in the business, the company used the cash to pay $150 million in dividends to its common shareholders; repurchase $135 million worth of its common stock and make $62 million in restructuring payments during the year. In comparison to the prior year, free cash flow was lower primarily due to the timing of working capital requirements.

Fourth Quarter 2015 Results

Revenue totaled $937 million, a decline of 2 percent on a constant currency basis and 5 percent on a reported basis when compared to the prior year.

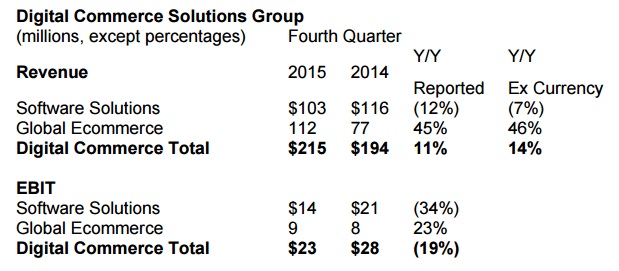

Revenue benefited from 14 percent growth on a constant currency basis and 11 percent growth on a reported basis in the Digital Commerce Solutions group, driven by growth in Global Ecommerce offset partially by lower results in the Software segment.

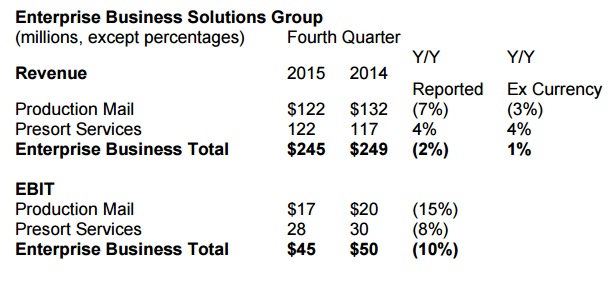

Revenue in the Enterprise Business Solutions group grew 1 percent on a constant currency basis and declined 2 percent on a reported basis. This resulted from continued growth in Presort Services offset by a decline in Production Mail.

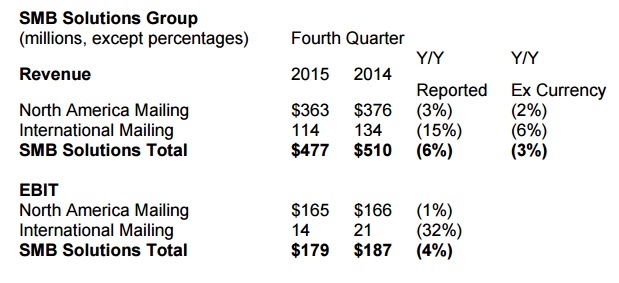

In the Small and Medium Business (SMB) Solutions group, revenue declined 3 percent on a constant currency basis and 6 percent on a reported basis. North America Mailing had a decline of only one percent for equipment sales in the U.S. compared to the prior year. Total revenue for International Mailing had the lowest rate of decline on a constant currency basis since the implementation of the new go-to-market strategy.

On a GAAP basis, earnings per diluted share were $0.44 for the fourth quarter.

Adjusted earnings per diluted share from continuing operations were $0.48 and exclude:

- $0.02 of expenses related to the exit of certain geographic markets during the quarter;

- $0.05 for restructuring charges and asset impairments;

- $0.03 of income from discontinued operations.

Earnings per share this quarter were reduced by $0.02 due to the impacts of foreign exchange.

Free cash flow during the quarter was $157 million, which was similar to the prior year. The company generated $164 million of cash from operations on a GAAP basis. The company used the cash to pay $37 million in dividends to its common shareholders; repurchase $35 million worth of its common stock and make $16 million in restructuring payments.

The company’s results for the quarter and full year are summarized in the table below:

* The sum of the earnings per share may not equal the totals above due to rounding. (Click on image to enlarge)

Debt Management

During the year, the company paid down $280 million of debt using cash on the balance sheet and the issuance of commercial paper. In the fourth quarter, the company used funds from a new $150 million bank term loan to refinance $110 million of debt. In January 2016, the company obtained an additional $300 million of bank term loans and refinanced $371 million of debt that matured in January.

Business Segment Reporting

The company revised its business segment reporting in the second quarter 2015 for its Digital Commerce Solutions segment. The company’s business segment reporting reflects the clients served in each market and the way it manages these segments for growth and profitability. The primary reporting segment groups are the SMB Solutions group; the Enterprise Business Solutions group; and the Digital Commerce Solutions group.

The SMB Solutions group offers mailing equipment, financing, services and supplies for small and medium businesses to efficiently create mail and evidence postage. This group includes the North America Mailing and International Mailing segments. North America Mailing includes the operations of U.S. and Canada Mailing. International Mailing includes all other SMB operations around the world.

The Enterprise Business Solutions group provides mailing and printing equipment and services for large enterprise clients to process mail, including sortation services to qualify large mail volumes for postal worksharing discounts. This group includes the global Production Mail and Presort Services segments.

The Digital Commerce Solutions group provides customer engagement, customer information and location intelligence software; and solutions that facilitate global cross-border ecommerce transactions and shipping solutions for businesses of all sizes. This group includes the Software Solutions and Global Ecommerce segments.

The Other segment is comprised of the Imagitas marketing services business, which was sold on May 29, 2015.

(Click on image to enlarge)

North America Mailing

Revenue declined on a constant currency basis at a lesser rate than through the first nine months of the year. In the U.S., equipment sales declined one percent versus the prior year while recurring revenue streams continued to perform in-line with prior quarters. EBIT margin improved versus the prior year due to the mix of business and lower employee-related costs.

International Mailing

Revenue declined at its lowest rate all year, benefiting from improved equipment sales trends in most of the major Revenue declined at its lowest rate all year, benefiting from improved equipment sales trends in most of the major markets where the Company has completed the shift in its go-to-market strategy. Equipment sales revenue grew on a constant currency basis, driven in part by increased sales in the UK. In France, equipment sales declined at a lesser rate than in previous quarters as the new sales structure increased productivity. However, equipment sales growth was offset by a decline in the recurring revenue streams. During the quarter, the Company sold, or entered into agreements to sell assets and convert to a dealer model in Mexico, South Africa and five markets in Asia.

International Mailing’s EBIT margin declined versus the prior year due to the impact of currency on costs and reduced, higher-margin recurring stream revenue.

(Click on image to enlarge)

Production Mail

Revenue trends improved versus the prior two quarters and benefited from growth in inserting equipment sales, driven in part by the new Epic product line, and higher supplies revenue. Revenue was adversely impacted by fewer printer installations than the prior year. EBIT margin declined versus the prior year due to product mix and increased engineering investments.

Presort Services

Revenue benefited from higher volumes of First Class and Standard mail processed versus the prior year, as well as new client acquisitions. EBIT margin declined versus the prior year due in part to investments made to expand the network into two new U.S. markets.

(Click on image to enlarge)

Software Solutions

Revenue declined due to lower licensing revenues in the Americas and Europe. The Company has allocated additional resources to expand its channel reach and focus on several high-potential industries and solutions. EBIT margin declined as a result of the lower amount of licensing revenue, which has a high margin.

Global Ecommerce

Results included a full quarter of revenue from Borderfree and growth in UK marketplace revenue. A number of new retail clients and expanded payment options also added to revenue in the quarter. However, outbound package shipments from the U.S. continued to be pressured by the strong U.S. dollar. This was especially true with regard to the Canadian and Australian dollars, which both declined in value by 15 percent versus the U.S. currency in comparison to the prior year. These markets represent two of the top three markets for volume shipped from the U.S.

EBIT margin declined versus the prior year due to the amortization of acquisition-related intangible assets, which offset the early stages of synergy savings.

The Other segment is comprised of the Imagitas marketing services business, which was sold in May 2015. (Click on image to enlarge)

2016 Guidance

This guidance discusses future results, which are inherently subject to unforeseen risks and developments. As such, discussions about the business outlook should be read in the context of an uncertain future, as well as the risk factors identified in the safe harbor language and as more fully outlined in the Company's 2014 Form 10-K Annual Report and other reports filed with the Securities and Exchange Commission.

This guidance excludes any unusual items that may occur or additional portfolio or restructuring actions, not specifically identified, as the company implements plans to further streamline its operations and reduce costs. This guidance also assumes that the global economy and foreign exchange markets in 2016 will not change significantly from year-end 2015 levels. Volatility in the foreign exchange markets could have a material effect on the company’s reported results compared to guidance. From a sensitivity perspective, for each 5 percent movement of the exchange rates material to the company’s business, reported revenue growth could be impacted by an approximately 150 basis point change and adjusted earnings per share could be impacted by about $0.03 per share.

The company expects in 2016:

- Revenue, excluding the impacts of currency; to be driven by growth in the double-digit range in Digital Commerce Solutions; flat to modest growth in Enterprise Business Solutions and a low single-digit decline in SMB Solutions.

- Revenue is expected to benefit from: the completion of the go-to-market shift in the Company’s major markets; new product launches across the portfolio; recent acquisitions, including Borderfree, Real Time Content (RTC) and Enroute Systems Corporation; the addition of new brands and retailers in ecommerce; the expansion of the Company’s Presort Services network.

- Ongoing improvement in SG&A as a percent of revenue as a result of the expected benefits from the implementation of the new ERP program. The majority of these benefits in 2016 are expected to be realized in the second half of the year, after the U.S. launch and stabilization period.

- Incremental Marketing expense related to the Company’s new advertising campaign that is expected to be the highest in the first and fourth quarters.

- A tax rate in the range of 32 to 35 percent.

Based on the above assumptions, the company’s 2016 guidance is as follows:

- Revenue, on a constant currency basis, is expected to be in the range of a 1 percent decline to 2 percent growth when compared to 2015.

- Earnings per diluted share from continuing operations to be in the range of $1.80 to $2.00 on both an adjusted and

GAAP basis. This guidance does not anticipate any potential adjustments to earnings. - Free cash flow to be in the range of $425 million to $525 million.

About Pitney Bowes

Pitney Bowes (NYSE: PBI) is a global technology company offering innovative products and solutions that enable commerce in the areas of customer information management, location intelligence, customer engagement, shipping and mailing, and global ecommerce. More than 1.5 million clients in approximately 100 countries around the world rely on products, solutions and services from Pitney Bowes. For additional information, visit Pitney Bowes at

www.pitneybowes.com.

Source: Pitney Bowes.