Amidst Cash Flow, Liquidity Concerns, Verso to Consider Reorganization, Asset Sales

MEMPHIS, Tenn.—November 16, 2015—In conjunction with the announcement of its third quarter financials, Michael A. Weinhold, senior vice president of sales, marketing and product development at Verso, addressed Verso customers in his letter below. Verso's financial results for the third quarter of 2015 are listed directly below the letter:

November 16, 2015

Dear Valued Customer,

Verso is currently facing a confluence of external factors that negatively affect our liquidity and cash flows, including impending financial obligations, an accelerated and unprecedented decline in demand for our coated paper products, and a significant increase in foreign imports resulting from a strong U.S. dollar relative to foreign currencies.

As a result of our cash flow and liquidity concerns, we have begun evaluating potential restructuring alternatives. Verso has engaged PJT Partners L.P. to provide us with restructuring and transactional services, and O'Melveny & Myers LLP to provide us with restructuring legal advice and assistance. We have also begun discussions with certain of our creditors to explore potential restructuring alternatives.

We also are exploring opportunities to raise funds through potential sales of some of our mills and related facilities, which may include our Stevens Point, Androscoggin and Duluth mills, our recently idled Wickliffe Mill, and the hydroelectric generation facilities associated with our Androscoggin Mill.

During this evaluation process, customers can expect to receive the same high-quality products and services that originally led them to select Verso as a supplier. There should be no changes or delays in the ordering process or deliveries, and customers should continue to work with their current sales representatives. We remain steadfastly committed to running our mills safely and efficiently, reducing costs and delivering the exceptional customer experience that Verso is known for.

As always, our aim is to ensure that all customer needs are seamlessly met. Please do not hesitate to call me if you have questions or concerns.

Thank you for your continued support of Verso.

Sincerely,

Michael A. Weinhold

Verso Corp. (OTCQB: VRSZ) reported financial results for the third quarter of 2015. Results for the quarters ended Sept. 30, 2015, and 2014 include:

- Net sales of $782 million in the third quarter of 2015 compared to $350 million in the third quarter of 2014.

- Operating income before special items of $23 million in the third quarter of 2015 compared to $16 million in the third quarter of 2014.

- Adjusted EBITDA of $84 million in the third quarter of 2015, compared to $41 million in the third quarter of 2014.

Overview

Verso's net sales for the third quarter of 2015 increased $432 million, or 123 percent, compared to the third quarter of 2014, due primarily to the addition of net sales resulting from the NewPage acquisition. However, when compared to 2014 sales as adjusted to include the impact of the NewPage acquisition and the sale of the Bucksport mill, Verso's sales have declined, quarter over quarter, reflecting an increase in offshore imports and a decline in U.S. demand for coated papers.

During the third quarter of 2015, Verso recorded special items affecting operating income totaling $66 million, or $0.80 per diluted share, primarily related to restructuring costs associated with the production capacity reduction and optimization of the Androscoggin mill and the indefinite idling of the Wickliffe mill, and integrating the legacy Verso and NewPage operations. During the third quarter of 2014, special items affecting operating income were $2 million, or $0.04 per diluted share.

"Despite continuing soft market conditions, Verso saw seasonal volume increases in the third quarter, particularly in coated freesheet," said Verso President and CEO David Paterson. "In response to a continuing decline in demand and oversupply of products, we decided to downsize our Androscoggin mill and indefinitely idle our Wickliffe mill, which together will reduce Verso's production capacity by 430,000 tons of coated paper and 130,000 tons of dried market pulp. We also took 79,000 tons of market-related downtime across our mill system during the third quarter."

Paterson continued, "In the face of these challenges, our employees remained focused on improving efficiency, reducing costs, and increasing job safety (achieving double-digit percentage reductions in recordable and lost time injuries). Verso also successfully fulfilled its financial obligations, paying $118 million in interest on our indebtedness during the third quarter. Despite these important achievements, and as we explain further in this press release, we intend to pursue a restructuring of our balance sheet to address our continuing cash flow and liquidity concerns."

Summary Results

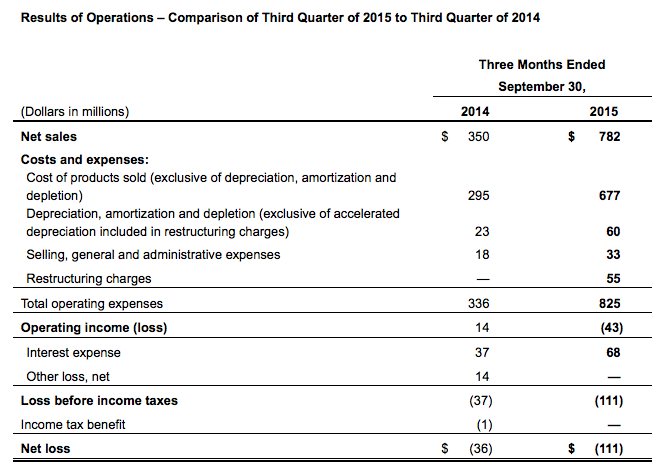

Net Sales. Net sales for the third quarter of 2015 increased 123 percent to $782 million from $350 million in the third quarter of 2014. Verso's sales increase was primarily driven by a 110 percent increase in total sales volume—from 433 thousand tons in 2014 to 910 thousand tons in 2015. The increase in volume resulted in $398 million of additional revenue, while changes in pricing contributed $34 million, as the average sales price per ton increased from $808 to $859, for all of its products in the third quarter of 2015, compared to the third quarter of 2014. When compared to 2014 sales as adjusted to include the impact of the NewPage acquisition and the sale of the Bucksport mill, Verso's sales have declined, quarter over quarter, reflecting an increase in offshore imports and a decline in U.S. demand for coated papers.

Net sales for Verso's paper segment increased 135 percent to $736 million in the third quarter of 2015 from $313 million in the third quarter of 2014, due to a 124 percent increase in paper sales volume to 829 thousand tons in the third quarter of 2015, compared to 371 thousand tons in the third quarter of 2014, supplemented by a 5 percent increase in average sales price per ton of paper to $888 in the third quarter of 2015, compared to $845 in the third quarter of 2014. The increased sales volume, which is primarily due to the addition of sales resulting from the NewPage acquisition, resulted in $387 million of additional revenue, which was augmented by the impact of changes in market pricing and product mix of $36 million.

Net sales for Verso's pulp segment increased 24 percent in the third quarter of 2015 to $46 million from $37 million in the third quarter of 2014, due to a 31 percent increase in pulp sales volume to 81 thousand tons in the third quarter of 2015, compared to 62 thousand tons in the third quarter of 2014, while the average sales price per ton declined 4 percent to $566 in the third quarter of 2015, compared to $589 in the third quarter of 2014. The increased sales volume, which is primarily attributable to the addition of net sales as a result of the NewPage acquisition, contributed $11 million of additional revenue, while the change in market pricing resulted in a decrease in revenue of $2 million.

Cost of sales. Cost of products sold, excluding depreciation, amortization and depletion expenses, increased $382 million, or 130 percent, in the third quarter of 2015, compared to the third quarter of 2014, primarily due to incremental costs as a result of the NewPage acquisition. Verso's gross margin percentage was 13.4 percent for the third quarter of 2015, compared to 15.8 percent for the third quarter of 2014, reflecting an incremental $49 million in gross margin, with $59 million attributable to volume increases offset by $10 million attributable to lower margin per ton. During the third quarter of 2015, Verso's margin per ton was negatively impacted by incremental costs related to mill maintenance outages and 79,000 tons of downtime. Depreciation, amortization and depletion expenses increased $37 million, or 161 percent, in the third quarter of 2015, compared to the third quarter of 2014, also primarily due to incremental costs as a result of the NewPage acquisition.

Selling, general and administrative. Selling, general and administrative expenses increased primarily due to incremental expenses of $15 million, or 83 percent, in the third quarter of 2015, compared to the third quarter of 2014, as a result of the NewPage acquisition. As a percentage of sales, selling, general and administrative expenses decreased from 5 percent in the third quarter of 2014 to 4 percent in the third quarter of 2015.

Restructuring charges. Restructuring charges of $55 million during the third quarter of 2015 consisted primarily of $35 million of noncash charges related to Verso's Androscoggin mill, and $15 million of severance and benefit costs related primarily to the production capacity reductions at its Androscoggin and Wickliffe mills.

Interest expense. Interest expense for the third quarter of 2015 was $68 million, compared to $37 million for the third quarter of 2014. The change in interest expense reflects the addition of the NewPage ABL Facility and NewPage Term Loan Facility, the 2015 First Lien Notes issued in connection with the NewPage acquisition, and changes resulting from the completion of the second lien and subordinated notes exchange offers.

Net Sales. Net sales for the nine months ended Sept. 30, 2015 increased 144 percent to $2,366 million from $970 million in the nine months ended Sept. 30, 2014. Verso's sales increase was primarily driven by a 126 percent increase in total sales volume, from 1,212 thousand tons in 2014 to 2,742 thousand tons in 2015. The increase in volume resulted in $1,267 million of additional revenue. The revenue increase associated with the increased volume was enhanced by the impact of pricing improvements of $128 million, as the average sales price per ton increased from $801 to $863, for all of its products in the nine months ended Sept. 30, 2015, compared to the nine months ended Sept. 30, 2014. When compared to 2014 sales as adjusted to include the impact of the NewPage acquisition and the sale of the Bucksport mill, Verso's sales have declined, on a year-to-date basis, reflecting an increase in offshore imports and a decline in U.S. demand for coated papers.

Net sales for Verso's paper segment increased 159 percent to $2,207 million in the nine months ended Sept. 30, 2015 from $851 million in the nine months ended Sept. 30, 2014, due to a 143 percent increase in paper sales volume to 2,456 thousand tons in the nine months ended Sept. 30, 2015 compared to 1,011 thousand tons in the nine months ended Sept. 30, 2014, supplemented by a 7 percent increase in average sales price per ton of paper to $898 in the nine months ended Sept. 30, 2015, compared to $842 in the nine months ended Sept. 30, 2014. The increased sales volume, which is primarily due to the addition of sales resulting from the NewPage acquisition, resulted in $1,217 million of additional revenue, which was augmented by the impact of changes in market pricing and product mix of $138 million.

Net sales for Verso's pulp segment increased 34 percent in the nine months ended Sept. 30, 2015 to $159 million from $119 million in the nine months ended Sept. 30, 2014, due primarily to a 43 percent increase in pulp sales volume to 285 thousand tons in the nine months ended Sept. 30, 2015, compared to 200 thousand tons in the nine months ended Sept. 30, 2014. The average sales price per ton declined 6 percent to $558 in the nine months ended Sept. 30, 2015, compared to $593 in the nine months ended Sept. 30, 2014. The increased sales volume, which is primarily attributable to the addition of net sales as a result of the NewPage acquisition, contributed $50 million of additional revenue, while a reduction of market pricing resulted in a decrease in revenue of $10 million.

Cost of sales. Cost of products sold, excluding depreciation, amortization and depletion expenses, increased $1,189 million, or 136 percent, in the nine months ended Sept. 30, 2015, compared to the nine months ended Sept. 30, 2014, primarily due to incremental costs as a result of the NewPage acquisition. Verso's gross margin was 12.8 percent for the nine months ended Sept. 30, 2015, compared to 10.0 percent for the nine months ended Sept. 30, 2014, reflecting an incremental $206 million in gross margin, with $122 million attributable to volume increases and $84 million attributable to higher margin per ton as a result of a different mix of paper products from NewPage. Depreciation, amortization and depletion expenses increased $107 million, or 145 percent, in the nine months ended Sept. 30, 2015, compared to the nine months ended Sept. 30, 2014, primarily due to incremental costs as a result of the NewPage acquisition.

Selling, general and administrative. Selling, general and administrative expenses increased primarily due to incremental expenses of $81 million, or 153 percent, as a result of the NewPage acquisition, in the nine months ended Sept. 30, 2015, compared to the nine months ended Sept. 30, 2014. As a percentage of sales, selling, general and administrative expenses were flat at 6 percent for the nine months ended Sept. 30, 2015 and 2014, respectively.

Restructuring charges. Restructuring charges for the nine months ended Sept. 30, 2015 were $83 million, and consisted primarily of $35 million of noncash charges related to its Androscoggin mill, $15 million of severance and benefit costs related primarily to the production capacity reductions at its Androscoggin and Wickliffe mills, $16 million of severance and benefit costs related to efforts to integrate the legacy Verso and NewPage operations, and $12 million of expenses related to the sale of the Bucksport mill.

Interest expense. Interest expense for the nine months ended Sept. 30, 2015 was $201 million, compared to $107 million for the same period in 2014. The change in interest expense year over year reflects the addition of the NewPage ABL Facility and NewPage Term Loan Facility, the 2015 First Lien Notes issued in connection with the NewPage acquisition, and changes resulting from the completion of the second lien and subordinated notes exchange offers.

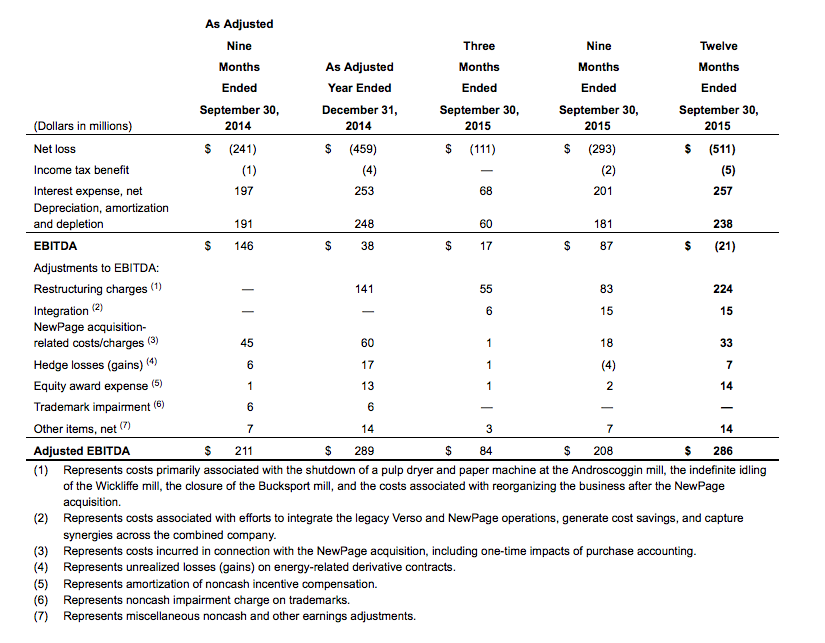

Reconciliation of Net Income to Adjusted EBITDA

EBITDA consists of earnings before interest, taxes, depreciation and amortization. Adjusted EBITDA reflects adjustments to EBITDA to eliminate the impact of certain items it does not consider indicative of ongoing performance. Adjusted EBITDA is a financial term commonly used in the industry. Verso uses Adjusted EBITDA as a way of evaluating its performance relative to that of its peers. The company believes that Adjusted EBITDA is an operating performance measure that provides investors and analysts with a measure of ongoing operating results unaffected by differences in capital structures, capital investment cycles, and ages of related assets among otherwise comparable companies.

Prior periods have been adjusted to include the historical operations of NewPage, excluding the Biron and Rumford mills, and to exclude the historical operations of the Bucksport mill. Verso encourages you to evaluate each adjustment and to consider whether the adjustment is appropriate. In addition, in evaluating Adjusted EBITDA, you should be aware that in the future, Verso may incur expenses similar to the adjustments included in the presentation of Adjusted EBITDA. The company believes that the supplemental adjustments applied in calculating Adjusted EBITDA are reasonable and appropriate to provide additional information to investors. Verso also believes that Adjusted EBITDA is a useful measurement tool for assessing its ability to meet its future debt service, capital expenditures, and working capital requirements.

Verso's debt agreements allow further adjustments to Adjusted EBITDA for the purpose of calculating covenant compliance. These additional adjustments include projected pro forma effects of its profitability program and, for Verso Holdings only, the pro forma impact of expected synergies related to the NewPage acquisition. Because EBITDA and Adjusted EBITDA are not measurements determined in accordance with accounting principles generally accepted in the United States of America, or "GAAP," and are susceptible to varying calculations, EBITDA and Adjusted EBITDA, as presented, may not be comparable to other similarly titled measures presented by other companies. You should consider our EBITDA and Adjusted EBITDA in addition to, and not as a substitute for, or superior to, our operating or net income or cash flows from operating activities, which are determined in accordance with GAAP.

The following table reconciles net (loss) income to EBITDA and Adjusted EBITDA for the periods presented as adjusted to include the historical operations of NewPage, excluding the Biron and Rumford mills, and to exclude the historical operations of the Bucksport mill:

Potential Restructuring and Asset Sales

Based on Verso's current liquidity position and its projections of operating results and cash flows for the remainder of 2015 and 2016, the company anticipates that it will not have sufficient resources to fund its most significant future cash obligations and, therefore, it believes that there is substantial doubt about its ability to continue as a going concern in the absence of a restructuring of its balance sheet. As a result of its cash flow and liquidity concerns, it has begun evaluating potential restructuring alternatives. Verso has engaged PJT Partners L.P. to provide it with restructuring and transactional services and O'Melveny & Myers LLP to provide it with restructuring legal advice and assistance.

Verso has have begun discussions with certain of its creditor constituencies to explore potential restructuring alternatives. It is also exploring opportunities to raise funds through potential sales of certain of its mills and related facilities, which may include the Stevens Point, Androscoggin and Duluth mills, its recently idled Wickliffe mill, and the hydroelectric generation facilities associated with its Androscoggin mill. Its potential restructuring could occur in a consensual, out-of-court manner or through a court-supervised Chapter 11 bankruptcy proceeding. While it intends to actively pursue a potential restructuring and potential asset sales, there can be no assurance that any of these activities will occur on terms acceptable to us or at all.

About Verso

Verso Corp. is the turn-to company for those looking to successfully navigate the complexities of paper sourcing and performance. The leading North American producer of printing and specialty papers and pulp, Verso provides insightful solutions that help drive improved customer efficiency, productivity, brand awareness and business results. Verso's long-standing reputation for quality and reliability is directly tied to its vision to be a company with passion that is respected and trusted by all. Verso's passion is rooted in ethical business practices that demand safe workplaces for itsr employees and sustainable wood sourcing for our products. This passion, combined with its flexible manufacturing capabilities and an unmatched commitment to product performance, delivery and service, make Verso a preferred choice among commercial printers, paper merchants and brokers, converters, publishers and other end users.

- Companies:

- Verso Corp.

{kind=link}

{kind=link}