EBITDA Trends in Printing and Packaging: Second Quarter Results

New Direction Partners compiles two charts that are published quarterly in Printing Impressions and packagePRINTING: the NDP Printing And Packaging EBITDA Trend Chart, and the NDP Printing And Packaging Stock Index. For now, let’s review the trend in EBITDA multiples for the two industry segments during the second quarter of 2015.

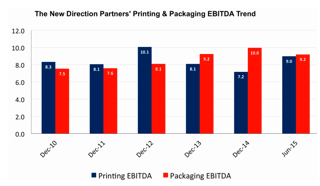

The chart tracks the EBITDA multiples of the top eight publicly traded printing companies and the top seven packaging firms. It shows the median multiples that these companies traded at between 2006 and today. What does the chart tell us? For both industries, there’s positive news, but the news probably is better if you are a printer rather than a packager.

Did we just say that news on the printing side is better than the news in packaging? That would be the first time in quite some time, and yes, it does appear to be the case. But as always, we need to look at the facts and some of the underlying numbers.

The chart shows that the median EBITDA multiple for printing increased very dramatically at the end of 2014 to the end of June of 2015, from 7.2 to 9. This does appear to be somewhat skewed, as one of the companies had a significant decline in earnings that wasn’t yet reflected in its stock price. What that ends up doing is artificially inflating the multiple.

That said, many of these stocks were up modestly over the six months, and that is a very healthy sign. This is one of the reasons why we are seeing higher multiples being paid in the acquisitions of privately held printers. On the packaging side, the median multiple was 9.2 at the end of June 2015 compared with 10 at the end of December 2014. This multiple therefore experienced a slight decline in the first half of 2015.

Nevertheless, the packaging segment continues to be very healthy and attractive on Wall Street. It’s growing, and we don’t see any reason for concern on the packaging side. The decline was merely a blip from some slightly lower earnings and stock prices that also had been reflected in the S&P 500 and the Dow Jones Industrial Average.

Besides demonstrating the disparity between printing and packaging, the chart also shows the ceiling for multiples that will be paid for privately held businesses. It also indicates why we are seeing transactions with multiples typically between 5 and 6.5 times EBITDA for printing and 6 and 7.5 times for packaging. Public companies will purchase a company only if it is accretive to earnings, meaning that they will need to pay a price at a multiple below the multiple they themselves are trading at. Otherwise, the transaction would be dilutive, and the buyer would be losing money.

So, if you’re trading publicly at 9.2 times EBITDA, the median for packaging, then you can easily afford to pay 7 times EBITDA. For printing, if you’re trading in the neighborhood of 7 or 7.5 times EBITDA, then you may be comfortable with a multiple of 6, but probably not a multiple of 7.5, because it would be dilutive.

That’s the snapshot at the end of the first half of the year—a picture that can and will change. Be sure to follow our quarterly indices in Printing Impressions and packagePRINTING to keep regular tabs on stock and valuation trends in both segments of the industry.

Peter Schaefer, partner at New Direction Partners, is an experienced dealmaker with more than 25 years of investment banking and valuation experience, 20 of which has been focused exclusively on the printing and packaging industries. He has closed more than one hundred transactions in virtually every segment of the printing and packaging industries. In addition, he has performed hundreds of valuations for ESOPs, estate and gift tax planning and strategic planning purposes. Contact him at (610) 230-0635, ext. 701.

{kind=link}